The 4 percent rule has come under scrutiny because of lower expectations about future security returns. Monte Carlo simulations using expected asset class risks and returns that reflect the current economy show that the first-year withdrawal can be 3.75 percent and increased for inflation each year. At 3.75 percent, portfolios with a 60 percent or higher equity exposure give a 90 percent chance of “spending success” over 30 years.

The cash proceeds from various reverse mortgage plans can be taken in different ways. Scheduled monthly tax-free advances reduce the need for portfolio withdrawals and can give better “spending success” levels than line-of-credit draws.

The increase in spending success levels depends on the relative value of the home and the portfolio. Given a portfolio value, higher home values raise success rates.

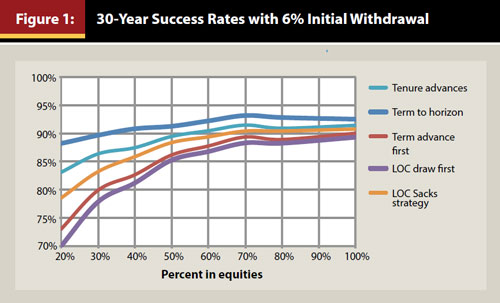

With a 30-year spending horizon and first-year withdrawal of 6.0 percent, reverse mortgage scheduled advances as a portfolio supplement give “spending success” levels of 88 to 92 percent. Even with a first-year withdrawal of 6.5 percent, success levels are still 83 to 86 percent. This paper provides financial planners with a review of the relative merits of using a reverse mortgage as a retirement spending supplement.

https://www.onefpa.org/journal/Pages/The%206.0%20Percent%20Rule.aspx