by Shaun Pfeiffer, Ph.D.; John Salter, Ph.D., CFP®, AIFA®; and Harold Evensky, CFP®, AIF®

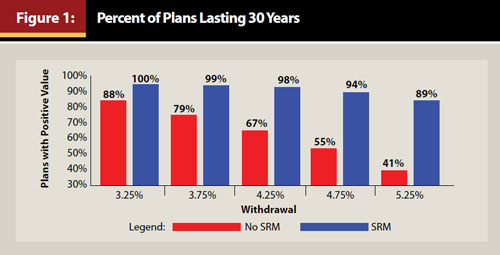

This study investigates maximum real sustainable withdrawal rates (SWRs) for retirement plans that incorporate the use of standby reverse mortgages (SRMs). The SWR is defined as the maximum real withdrawal rate with a minimum 90 percent plan survival rate for a 30-year retirement horizon.

The SRM evaluated in this study is a Home Equity Conversion Mortgage (HECM) reverse mortgage line of credit that is established at the beginning of retirement and is used for retirement income during bear markets. Outstanding loan balances are repaid from the Investment Portfolio (IP) in bull markets.

Monte Carlo simulations were used to estimate the success of the SRM strategy at various real withdrawal rates for a client who has a $500,000 investment nest egg and $250,000/$500,000 in home equity at the beginning of retirement. The $500,000 nest egg is split into a 60 percent stocks and 40 percent bonds IP and a six-month cash reserve.

Retirees who begin retirement in a low interest rate environment (2.3 percent yield on 10-year U.S. Treasury bond) with competitive lending terms and significant home equity relative to the IP stand to benefit the most from an SRM strategy. Interest rates and the size of the initial line of credit relative to the IP are the two factors that are shown to have a significant impact on the SWR for the SRM distribution strategy.