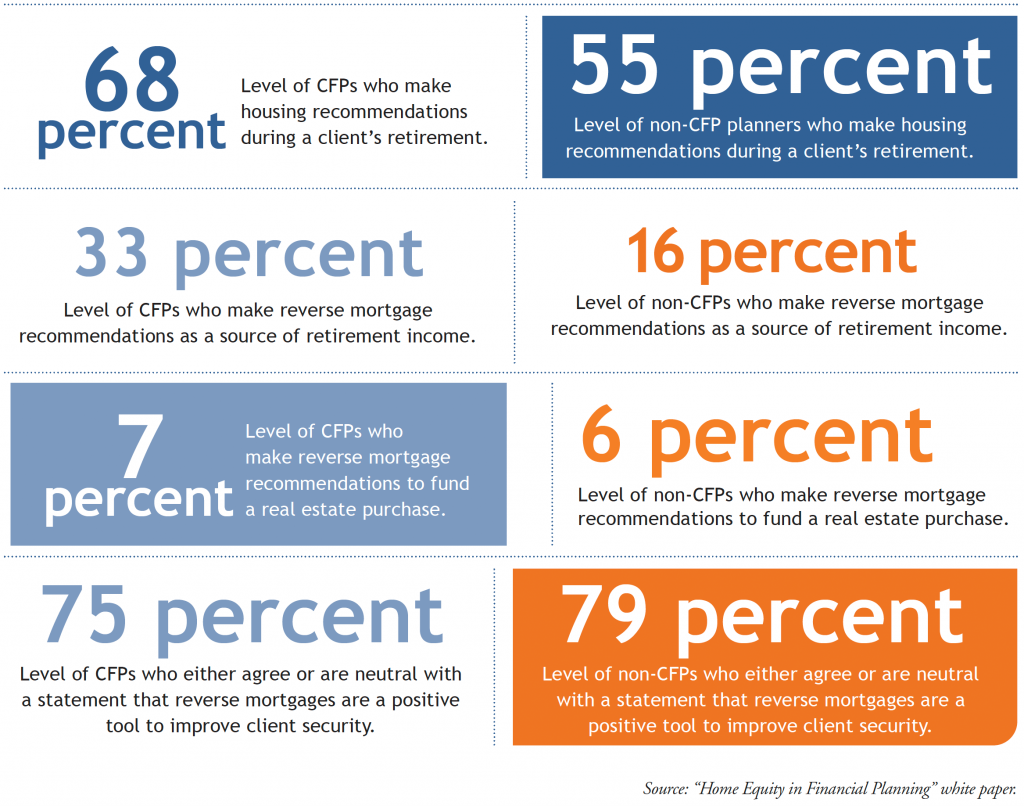

Numbers Indicate How Financial Planners Discuss Reverse Mortgages

In his white paper “Home Equity in Financial Planning,” Craig Lemoine, executive director of the Academy for Home Equity in Financial Planning at The University of Illinois at Urbana-Champaign, illustrates the need for home equity release programs. “The Academy of Home Equity in Financial Planning’s mission is to develop and advance, for retirees and their financial advisers, a rational and objective understanding of the role that housing wealth can play in prudent planning for retirement income,” says the 2020 report, which included detailed surveys of financial professionals. Lemoine also is an associate clinical professor of financial planning at the university. Here is a closer look at some of his findings that, in some cases, compare how a Certified Financial Planner operates compared to a non-CFP.

Whenever the subject of reverse mortgages come up, invariably one of the objections that are cited is the perceived high cost of originating a reverse mortgage. Virtually every news media article about reverse mortgages cites the high cost and how it eats away at equity. That is why so many advisors recommend they only be used as a “loan of last resort” when there is no other option.

The opposite is actually true. When all costs are considered, reverse mortgages became the loan of first resort. The fact is that they actually cost considerably less when used as a source of income as compared to a portfolio or continuing to make payments from a portfolio once past the age of 62. Let’s investigate the concerns that both consumers and advisors have about the actual fees and closing costs that are the subject of concern.

EquityAvail TM lowers monthly mortgage payments for ten years, at which time they are eliminated altogether; creates glidepath to retirement.

Innovative hybrid product, combines aspects of traditional and reverse mortgages to deliver a ‘new world of options’ for homeowners at or near retirement

For many Americans over the age of 60, the pathway to achieving financial security in retirement has become increasingly challenging. They are living longer and often have cashflow shortfalls and carry significant debt – including a traditional home mortgage. In fact, over the last three decades, the number of people over the age of 60 burdened by traditional mortgage debt has doubled to more than 40%i. With historically low interest rates, some homeowners will end up exploring a mortgage refinance in an effort to reduce monthly payments and potentially take “cash out” from their home equity. However, a traditional refi can spell trouble for borrowers over 60 who are charting their course to retirement.

When one or more borrowers have reduced income due to retirement, they may not qualify under traditional loan guidelines due to high debt-to-income ratios.

Those who do qualify can end up tethered to 30 more years of mortgage payments. If ability to make these mortgage payments is dependent upon continued full-time employment, this is not sustainable for borrowers hoping to retire.

Even if the borrowers can qualify for a refinance today, and plan to work for the foreseeable future, an unexpected income loss—through disability, death of a partner or unrelated economic upheaval, like that encountered in 2020 with COVID-19—could leave the borrowers with no feasible option but to sell their home.

The upcoming launch of EquityAvail by leading retirement solutions innovator Finance of America Reverse LLC (“FAR”) is opening up a significant new set of options for homeowners. This product is the first-of-its-kind and will provide a needed option for a large segment of the population looking to improve cashflow and remain in their home for as long as they wish.

COVID-19 created major new health risks for Americans at all ages and, at the same time, had a major impact on the economy and daily life, exacerbating a wide variety of retirement risks. The retirement system faced major challenges before the pandemic, but the pandemic and its consequences may change the way people look at retirement issues. This article reviews how COVID-19 changed the economic environment, the work environment and the situation for retirees. It provides insights into employer responses to date and a discussion about what they might do in the future. Organizations that make major changes in employment strategies will also need to revisit their retirement benefits strategies. This article further provides a discussion of retirement risks based on recent Society of Actuaries (SOA) research and includes COVID-19 impacts on the risks. It brings together consideration of retirement risks, the environment before COVID-19, changes in that environment and possible future directions for retirement benefits. In 2020, SOA released a new version of its “Post-Retirement Risk Chart” and several reports on retirement risk and COVID-19. These reports were also used to inform this article.

Many people experience cognitive and/or physical decline as they age. Their first source of support when they need help is often the family, including their adult children. Caregiving adult children are often employed, and helping with the needs of their parents or other family members can impact their ability to perform their own jobs. Society of Actuaries (SOA) research provides insights about the challenges facing aging Americans and the impact these challenges have on their adult children. This article will highlight implications for employers and present ideas for helping employees deal with these issues as part of their financial wellness programs.

By Jamie Hopkins and Dr. Craig Lemoine on February 10, 2021

The Academy for Home Equity in Financial Planning at the University of Illinois at Urbana-Champaign believes that certain retirees can have a more secure retirement when home equity is used prudently. The Academy has just released compliance guidance around home equity and financial planning designed to help financial service companies update their language, policies, and procedures, many of which no longer follow best practices in the industry.

The Academy for Home Equity in Financial Planning at the University of Illinois at Urbana-Champaign believes that certain retirees can have a more secure retirement when home equity is used prudently.

The average pre-retiree and retiree in the U.S. today have under-saved and risk running out of money in retirement. According to the Census Bureau, home equity represents roughly two-thirds of the net worth of the average American age 65 and over. A reverse mortgage could be an appropriate solution for those who want to stay in their homes and would prefer more cash flow to pay bills or unexpected expenses. Using housing wealth during market downturns can also improve financial outcomes in retirement by protecting investment portfolios from sequence of returns risk. Prudent use of home equity in a holistic retirement plan – where all the client’s assets as considered for their retirement security – helps advisors serve their client’s best interests and the client’s need for retirement savings to last a lifetime.

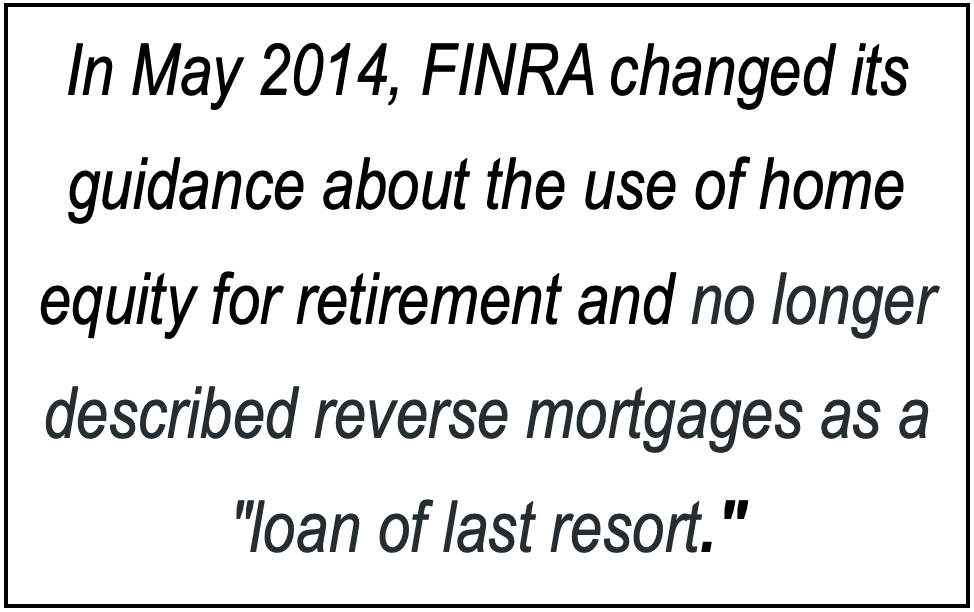

Many broker-dealers and financial service firms maintain that a reverse mortgage is appropriate only as a last resort once all other available assets are depleted. There is no evidence that this is the case. Some firms and advisors are not aware that in May 2014, FINRA changed its guidance about the use of home equity for retirement and no longer describes reverse mortgages as a “loan of last resort.”

Several broker-dealers and other advisory firms recently discontinued their prohibition on reverse mortgages and adopted more reflective compliance policies around the current state of the role of reverse mortgages and home equity. They believe their trusted advisors should understand how the product works, its potential solutions, and advise and educate clients effectively to make decisions best suited to their needs and circumstances. They believe that if their advisors are restricted from advising or educating clients on the topic of reverse mortgages and retirement housing planning, they are not serving their clients’ best interests.

It remains up to each compliance department, company, and advisor to set their policies. However, if an advisor is engaged in financial planning and a client wants to consider their plan with and without a reverse mortgage, that advisor should provide the resources to do so. According to FINRA, “Home equity is often a homeowner’s most valuable asset and most precious source of retirement security. Reverse mortgages can be a useful tool for certain older Americans who might otherwise face losing their homes. But homeowners should consider all the risks and explore all of their options before taking out a reverse mortgage, and even then, should use the loan funds wisely.”

Today, many firms’ policies are out of date and limit clients’ ability to get education or advice from their trusted advisor about reverse mortgages. The Academy of Home Equity in Financial Planning has reviewed several broker-dealers and advisory firms’ compliance policies. We offer the following Model Language currently being used by RIAs, broker-dealers, and other advisory firms to help you create or modify existing policies regarding reverse mortgages when updating or replacing existing guidance provided by your firm.

Proposed Guidance on Reverse Mortgage Compliance Policies

A reverse mortgage is a non-recourse loan secured by the home, in which monthly principal and interest payments are not required. Unpaid interest accrues on the loan balance and compounds. The loan proceeds are available as a lump sum (often used to refinance a current mortgage), a monthly payment stream, or a Line of Credit, or a combination.

Advisors and firms may discuss the benefits and drawbacks of a reverse mortgage with clients and provide approved educational materials on the topic.

Advisors are prohibited from soliciting, recommending, or advising a client to use reverse mortgage proceeds to fund securities or insurance products. If a client indicates that he has proceeds from a reverse mortgage for investing, contact Compliance immediately. The solicitation (sale) of a reverse mortgage is a prohibited activity at the firm.

For an advisor or registered representative to advise a client to engage in a reverse mortgage to improve their retirement income outcomes or other stated financial planning objectives, the client must have signed a financial planning agreement. If a RRs/IARs decides to recommend a reverse mortgage product, they must recommend at least three FHA-approved reverse mortgage lenders.

Any conflicts of interest must be disclosed in writing to the client as it relates to the recommendation of any mortgage product, including a reverse mortgage.

More than 90% of reverse mortgages in use are the Home Equity Conversion Mortgage (HECM) and are administered by the Federal Housing Administration (FHA). Loan terms are strictly regulated by FHA and the loan is non-recourse, meaning that neither the homeowner nor his estate can be held liable for a loan amount beyond the value of the house. The loan, even in the credit line format, cannot be arbitrarily canceled, frozen, or reduced by the lender.

The safeguards inherent in the HECM are insured by FHA through borrower premiums that accrue on the loan amount.

RRs/IARs may discuss, model, and recommend a HECM in a financial plan if it is advisable for the client based upon the totality of the client’s facts and circumstances and in light of applicable suitability and best interest standards.

RRs/IARs are permitted to assist a client through the reverse mortgage transaction process, helping to collect paperwork and attending meetings. However, while RR/IARs can attend the client’s meeting(s) with the reverse mortgage lender, they must not be an active participant in the meeting.

PROVIDING REVERSE MORTGAGE EDUCATION FOR CONSUMERS

What is a Reverse Mortgage?

A reverse mortgage is an interest-bearing loan secured by the home. The most used reverse mortgage is the FHA-insured Home Equity Conversion Mortgage (HECM). To be eligible for the HECM, one homeowner must be 62. Younger spouses, known as “non-borrowing spouses” are allowed but benefits are reduced. Some lenders offer private reverse mortgages to individuals as young as age 60.

Like a home equity loan, a reverse mortgage allows you to convert your home equity to cash that you can use for any purpose. Unlike other home loans, however, homeowners are not required to make monthly interest or principal payments during the life of the loan. However, borrowers can choose to make voluntary payments to principal or interest to help manage the cost of the loan. Unpaid interest is added to the loan balance, which is why reverse mortgages are often called “rising debt” loans.

The HECM reverse mortgage loan typically only becomes due when you die, sell your home to move, or otherwise leave your home for more than 12 months—for instance, if a health issue requires the last remaining homeowner to enter a nursing home. (There are special provisions for non-borrowing spouses when the borrowing spouse exits the home that must be considered.)

The loan is due when the last homeowner is no longer using the home as a principal residence. Snowbirds are allowed. When the loan is terminated, you or your heirs must repay the loan which consists of draws, compound interest, FHA insurance premiums, and servicing fees, if any. The loan can be satisfied through the sale of the home, refinancing the loan, or payment from other assets, the same as most options available with traditional loans.

Because interest will have been accruing during the life of the loan, you will likely owe more than you borrowed—and if home values have fallen or you live longer than expected, the loan balance could exceed the home value. But since reverse mortgages are non-recourse loans, the worst that will happen is that you or your heirs will receive nothing from the sale of your house because the full amount of the sale proceeds went to repay the loan. The lenders cannot go after any other assets that you or your heirs own. For further information, read FINRA’s investor alert on reverse mortgages here.

Lenders are prohibited from arbitrarily canceling, freezing, or reducing the HECM loan benefits.

Your financial advisors can help determine what is in your best interest when it comes to financial planning and available strategies or products. Lending strategies, mortgages, and reverse mortgages can play an important part in your retirement income planning.

The Academy for Home Equity in Financial Planning took a deep dive into how financial planners work with and understand credit tools. This white paper is the result of a Spring 2020 survey of financial planners, insurance agents and registered representatives. The results shed light on how financial planners make credit recommendations, and how education enhances usage of credit products.

By Daniel Hunt, Lisa Shalett, Zi Ye, and Stephanie Wang on March 31, 2020

The answer to the question, “How prepared are you for retirement,” depends a lot on whether you look holistically at the balance sheet, including home equity, or just at the portfolio and income sources like Social Security. When home equity is ignored, that can cause households to make suboptimal decisions, such as forgoing longplanned spending it could afford or taking more investment risk than it’s comfortable with. When a questionable decision like that encounters the kind of market downturn we are currently experiencing, it can do serious damage to household finances and well-being.